Delve Tech Due Diligence · Meta-Analysis

Cloud Infrastructure Landscape

AWS dominance, PaaS-first patterns, and platform concentration risk

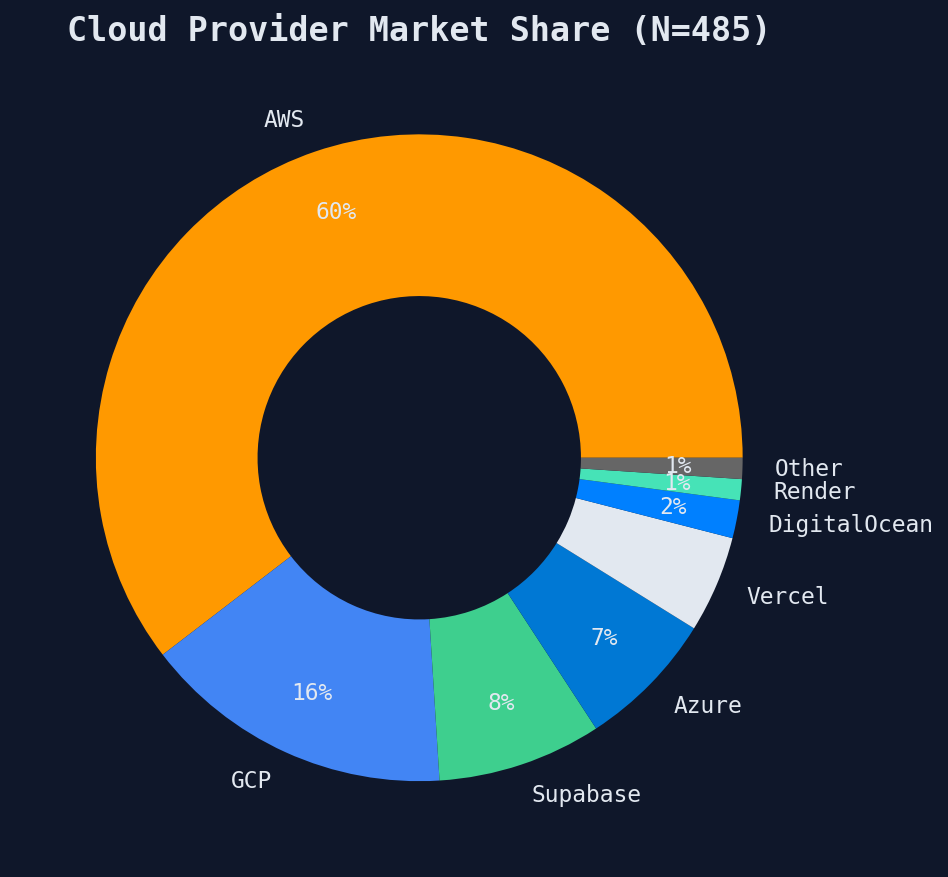

287

AWS (59%)

74

GCP (15%)

39

Supabase

23

Vercel

Market Share

| Provider | Companies | Share |

|---|---|---|

| AWS | 287 | 59.2% |

| GCP | 74 | 15.3% |

| Supabase | 39 | 8.0% |

| Azure | 33 | 6.8% |

| Vercel | 23 | 4.7% |

| DigitalOcean | 9 | 1.9% |

| Render | 5 | 1.0% |

| Other | 5 | 1.0% |

| Fly.io | 5 | 1.0% |

| Railway | 2 | 0.4% |

Systemic risk: 59% of the portfolio runs on AWS. A major AWS regional outage would simultaneously impact 287 companies.

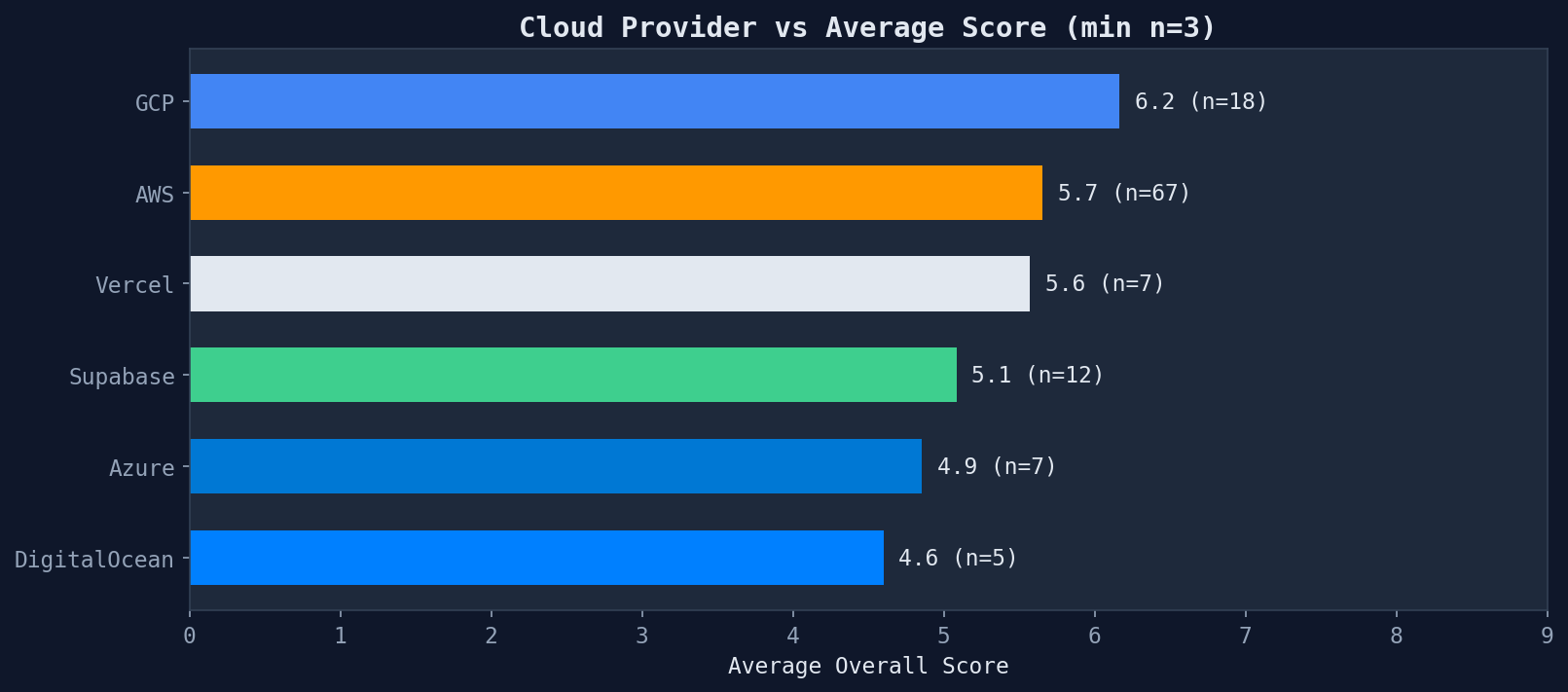

Cloud Provider vs Score

Does cloud provider choice predict tech maturity?

Cloud choice alone doesn't determine score — architecture decisions matter more than which cloud you're on. But PaaS-first companies tend to have simpler architectures with fewer disclosed features.

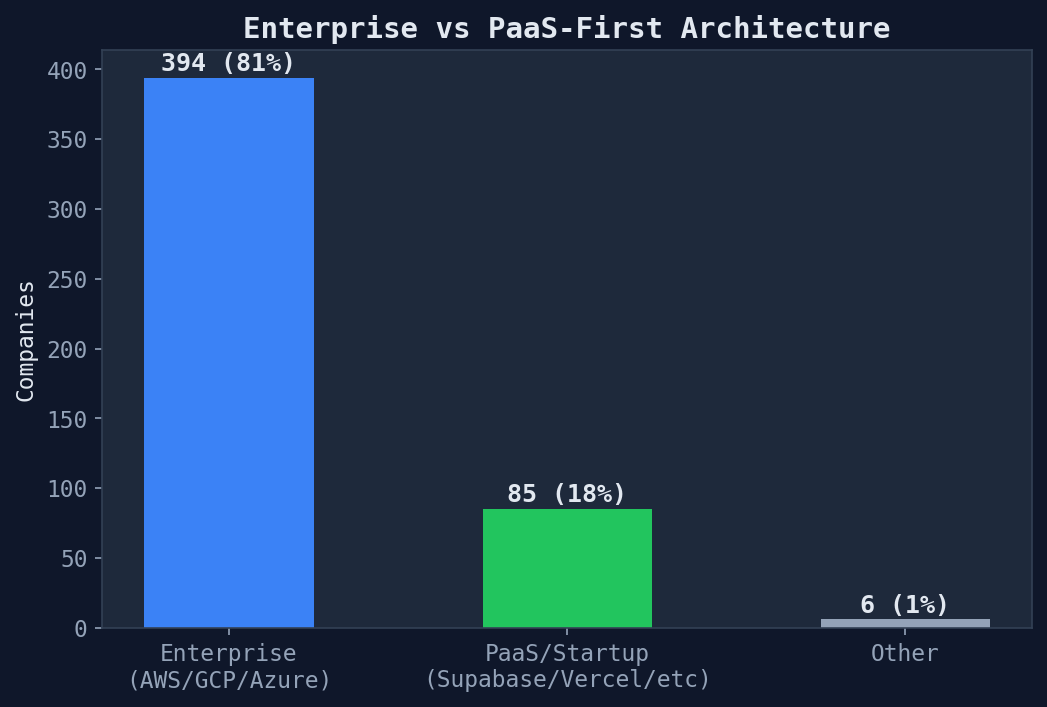

Enterprise vs PaaS-First

A clear divide exists between companies built on enterprise hyperscalers (AWS/GCP/Azure) and those using PaaS platforms (Supabase, Vercel, Render) as their primary infrastructure.

PaaS-First Implications

- Speed advantage: PaaS companies deploy faster with less ops overhead

- Control trade-off: Many controls are delegated via carve-out (not audited directly)

- Migration risk: Moving off Supabase/Vercel is harder than migrating between hyperscalers

- Scaling ceiling: PaaS platforms may not scale to enterprise workloads

Generated from cloud infrastructure landscape module · 485 SOC 2 compliance reports · 2026-03-24